PAYTM KARO? Pre-IPO Notes.

PAYTM KARO? Pre-IPO Notes.

Understanding and reviewing their business other important aspects.

Wassup Guys! This is Ankur here from Fruits Investments.

Today we review and understand the insights of our day-to-day life mobile application company. We will be discussing –

What all do they do?

How do they do it?

How much do they earn from it? Is it good or bad?

What is the point of doing all this research before applying for a company’s IPO?

It helps you understand their business, management, and business operations. We should always know where we are putting our hard-earned money. This also gives an edge to our investment decision-making. We should never invest a penny in a bad company.

Let’s get on with it!

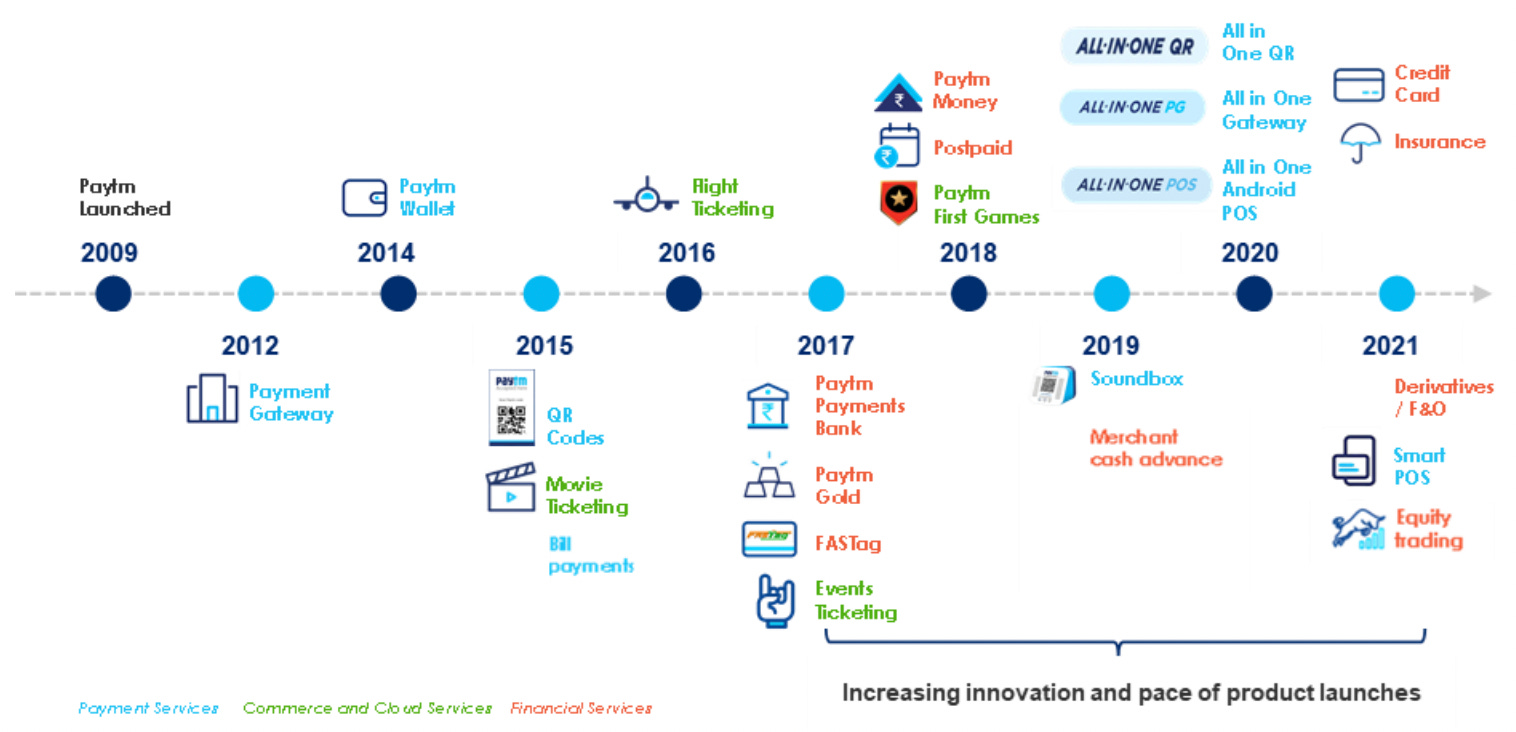

PAYTM is India’s leading digital ecosystem for consumers and merchants, according to RedSeer. They offer payment services, commerce and cloud services, and financial services to 333 million consumers and over 21 million merchants registered with them, as of March 31, 2021. Their two-sided (consumer and merchant) ecosystem enables commerce, and provides access to financial services, by leveraging technology to improve the lives of our consumers and help our merchants grow their businesses.

Their Future Prospects -

Incorporated in 2009 PAYTM has products and services like –

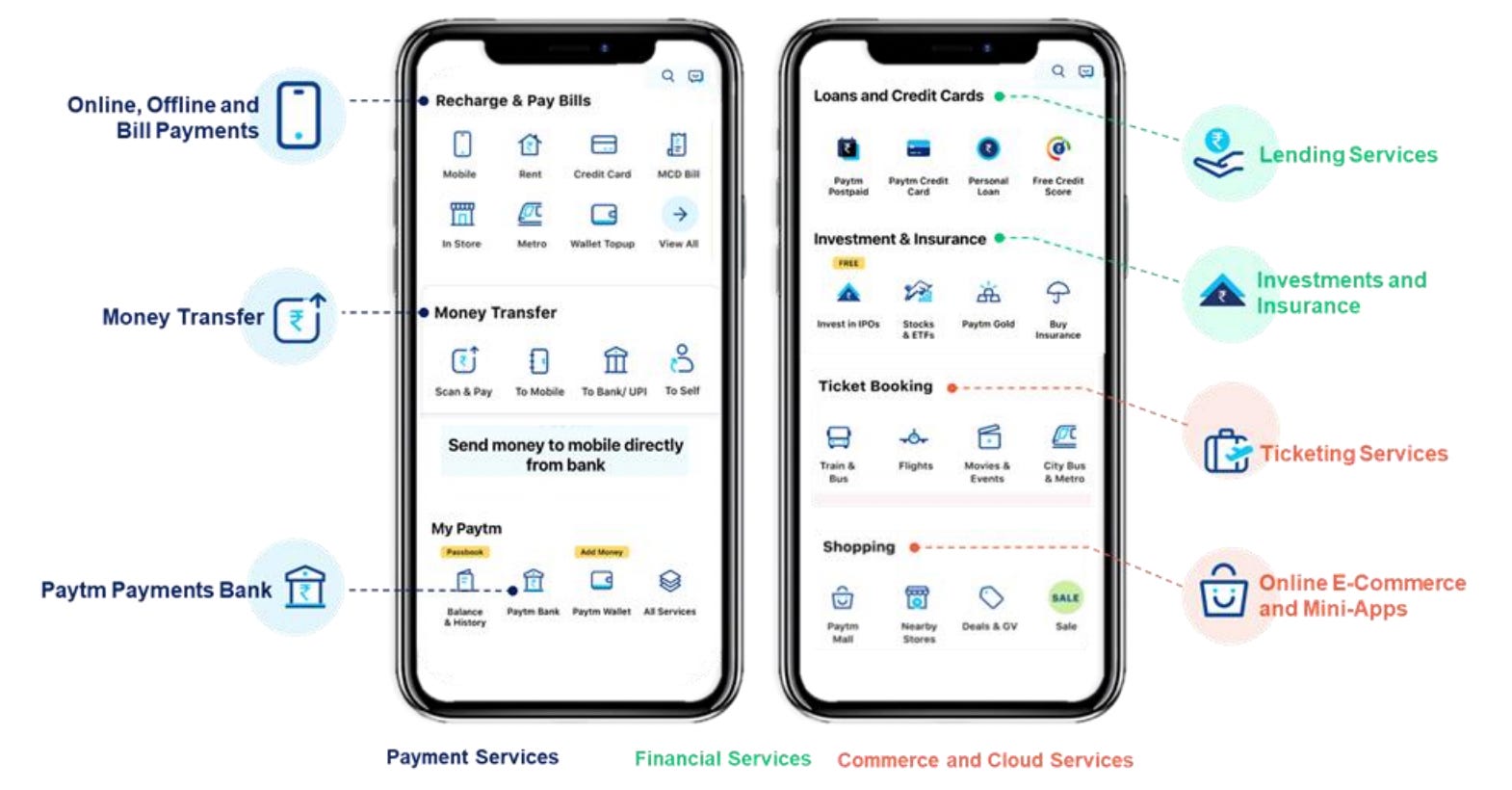

Paytm Super-app to access a wide selection of daily life use cases: Such as utility bill payments, mobile top-ups, money transfer, online and in-store payments, buying entertainment and travel tickets, playing online games, accessing mini-apps across content, food delivery, e-commerce, and ride-hailing, and doing other things.

Consumers benefit :

Usage of Paytm Payment Instruments: Such as Paytm Wallet, Paytm Postpaid, Paytm Debit Card, Paytm Credit Card, and others, which meet consumer needs such as convenience, trust, and transaction credit. These instruments can be used on online and mobile platforms, including on the Paytm app, as well as for in-store transactions, and are deeply integrated with the ecosystem.

Access to financial services through our partners: In partnership with financial institution partners, they provide their consumers and merchants, including unserved or underserved Indians with access to digital, customized financial products, such as deposits, wealth, lending, and insurance on the Paytm app. They have also made their experience of buying and using financial services and products instant, seamless, convenient, and completely digital.

Merchants Benefits :

Comprehensive payments solutions: Gives merchants the ability to accept payments, online and on mobile platforms, and in-store, from a wide selection of Paytm Payment Instruments and all major third-party instruments. Our new-age in-store payment systems offer an opportunity for merchants to integrate customer loyalty, gift vouchers, and buy-now-pay-later solutions. We also help merchants with products for seamless business payments to vendors, employees, and customers.

Acquisition and retention of customers and demand creation: helps merchants acquire and retain customers on and off the Paytm app, through their suite of products such as commerce, advertising, mini-app listings, channel, and loyalty solutions. These products allow merchants to leverage their large consumer base to: find new customers, retain existing customers, drive conversions and create demand for their products and services through targeted distribution strategies leveraging our rich insights.

Access to digital financial services: For unserved or underserved merchants, they offer them access to deposits, wealth, credit, and insurance products to improve and grow their businesses, including through their associates and partner financial institutions offer products and services across payment services, commerce, and cloud services, and financial services.

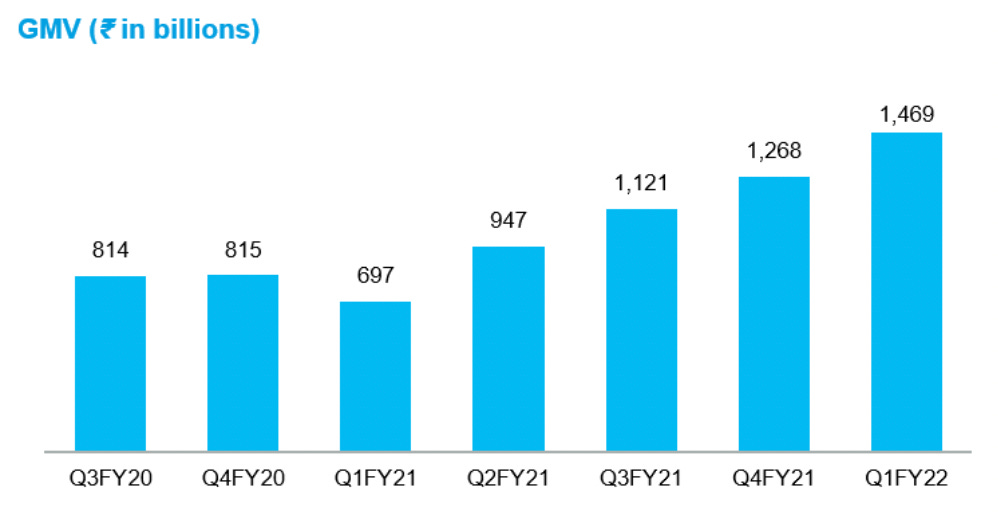

Payment Services According to RedSeer PAYTM is the largest payments platform in India with a GMV of ₹4,033 billion in FY 2021.

Have payments transaction volume market share of approximately 40%, and wallet payments transaction market share of 65% – 70% in India as of FY 2021, according to RedSeer.

PAYTM FOR BUSINESS:

COMMERCE & CLOUD SERVICES

TRAVEL TICKETING

ENTERTAINMENT TICKETING

ADVERTISING

GAMING

PAYTM FIRST – LOYALTY PROGRAM

ANDROID MINI APP PLATFORM FOR DEVELOPERS

SOFTWARE & CLOUD SERVICES:

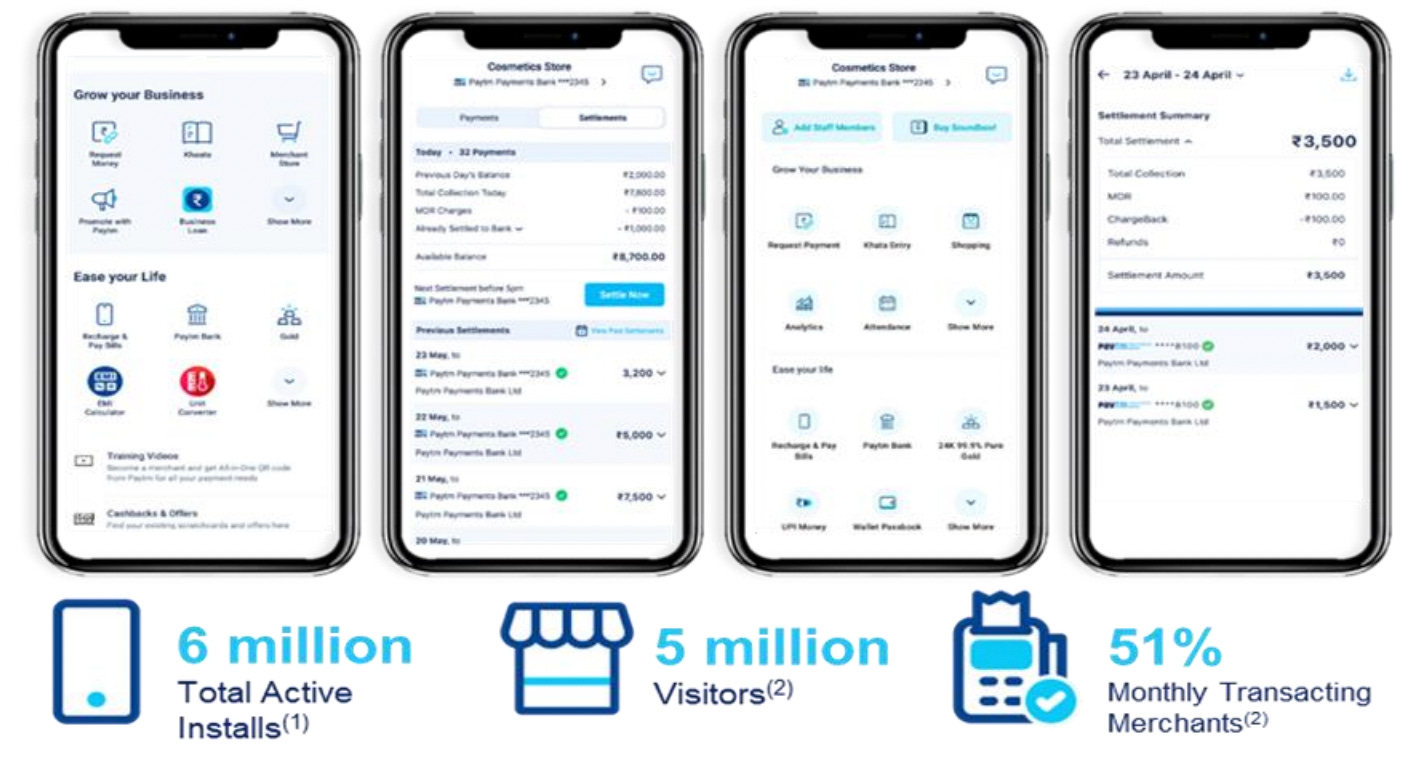

SMALL & MEDIUM ENTERPRISE CLOUD: Services include (i) Loyalty which enables merchants to issue cashback, vouchers, and other such deals to their customers as loyalty rewards. Users can redeem these rewards on the Paytm App, (ii) Channel which allows merchants to open an online storefront where they can directly communicate with their customers, and (iii) Billing and Ledger Services (Business Khata) which is an e-ledger service. Business Khata also provides additional services to merchants including the ability to (i) save customer details, (ii) record sales and payments, (iii) track customer balance instantly, and (iv) send direct payment links to customers.

ENTERPRISE: This offers a wide range of products and services in this segment to mobile consumers in over 24 countries and over 170 brands across the globe. Their products and services include platforms and solutions to manage customer lifecycle, digital services to engage consumers, and entertainment content to upsell customers.

PAYTM AI CLOUD (PAI CLOUD) : A proprietary suite of SaaS applications created in-house to address requirements of digital and fintech platforms ranging from building payments systems, preventing fraud, managing multi-channel customer engagement, and unlocking customer insights.

FINANCIAL SERVICES :

PAYTM PAYMENTS BANK: It provides banking services through Paytm Payments Bank, of which PAYTM owns 49% equity interest. Paytm Payments Bank holds a payments bank license from RBI. Paytm Payments Bank has the largest scale among all licensed Payments Banks in India, according to RedSeer, in terms of mobile transactions. As of March 31, 2021, Paytm Payments Banks had 64 million savings accounts, and over ₹52 billion deposits (including savings accounts, current accounts, fixed deposits with partner banks, and balance in wallets). As of March 31, 2021, over 50% of their registered merchants hold an account with Paytm Payments Bank and benefit from its new-age digital banking services.

Paytm Payments Bank is a mobile-first bank with no zero minimum-balance requirement for accounts and has no digital transaction charges or maintenance charges for the accounts. Paytm Payments Bank offers one of the most comprehensive suites of digital banking products, for individuals, small and medium enterprises, and large corporates which can be accessed directly by users through the Paytm app. Paytm Payments Bank is also one of India’s first payments banks to launch a video KYC facility, according to RedSeer, which provides a zero-contact and paperless KYC for consumers thereby helping improve customer acquisition spending.

Products offered by Paytm Payments Bank include:

PAYTM WALLET

PAYTM UPI

SAVINGS ACCOUNT

FIXED DEPOSIT

CORPORATE SALARY ACCOUNT

CURRENT ACCOUNT

DOMESTIC MONEY TRANSFER

TOLL TRANSIT

AADHAR ENABLED PAYMENT SYSTEM

NATIONAL AUTOMATED CLEARING HOUSE

PAYTM PAYMENTS BANK has a partnership with PAYTM MONEY to enable payment mandates for IPO for investors to use their @paytm UPI to invest in capital markets. Approved by SEBI.

PAYTM PAYMENTS BANK is a registered Bharat Bill Payment Operating Unit for customer transactions and processing transactions with more than 50 billers on-boarded on Bharat Bill Payment System across key categories such as utilities and financial services.

As per guidelines, PAYTM PAYMENTS BANK will be eligible for the license of SMALL FINANCE BANK in 2022 to (i)offer small-ticket loans, (ii) have no upper limit on bank account balance, and (iii) offer all deposit products such as non-resident Indian accounts and Fixed Deposits directly.

Paytm Payments Bank and Paytm Financial Services Limited (Group Company), make up the promoter group of Foster Payment Networks Private Limited (a nine-partner company consortium) which has applied to the RBI for authorization of setting up a New Umbrella Entity on March 31, 2021. As per the RBI guidelines, New Umbrella Entities are intended to manage and operate new payment systems, especially in the retail sector such as networks for ATMs, white-label PoS, Aadhar-based payments, and remittance services.

PAYTM PAYMENTS BANK also provides consumer lending like :

PAYTM POSTPAID - A BNPL service (Buy Now Pay Later) has a credit limit of up to ₹60,000 for a maximum of 30 days.

PERSONAL LOAN ranges from ₹10,000 to ₹200,000.

CREDIT CARDS: Offers Co-Branded Credit Cards

MERCHANT LENDING: Offers unsecured business loans credit-scored based on the transaction history of the merchant.

INSURANCE & ATTACHMENT PRODUCTS :

As of March 31, 2021, they, together with Paytm Insurance Broking Private Limited, had 11.3 million unique insurance customers and sold 31.5 million cumulative attachment products and insurance policies. Paytm Insurance Broking Private Limited currently has direct integration with 47 insurance companies in India.

Also Provides WEALTH MANAGEMENT SERVICES via PAYTM MONEY :

MUTUAL FUNDS: have over 1.3 million consumers, for direct mutual funds investments as of March 31, 2021

EQUITY TRADING: As of March 31, 2021, they had 208,000 equity trading accounts

GOLD: As of March 31, 2021, they had 74 million investors who have used the digital gold service since its launch in April 2017, with many opting for Gold systematic investment plans as a regular saving option. Recently, SEBI has issued a notice against all digital gold offering platforms to stop this service.

PAY PAY: incorporated under the laws of Japan in 2018. Provides Payment & Financial Services. PayPay had over 38 million users and 3.16 million registered locations accepting PayPay. For the year ended March 31, 2021, PayPay processed over 2 billion payment transactions with a value of over 3.2 trillion Japanese Yen.

Over FY 2021, PAYTM had an average of 8,623 on-roll employees worldwide.

GROWTH STRATEGIES :

Grow consumer and merchant base.

Expand and enhance Paytm App’s offerings for our consumers.

Deepen merchants’ partnerships and drive adoption of technology among our merchant base.

Rapidly scale up financial services and expand access to financial services through deep tech-led solutions.

Expand into international markets.

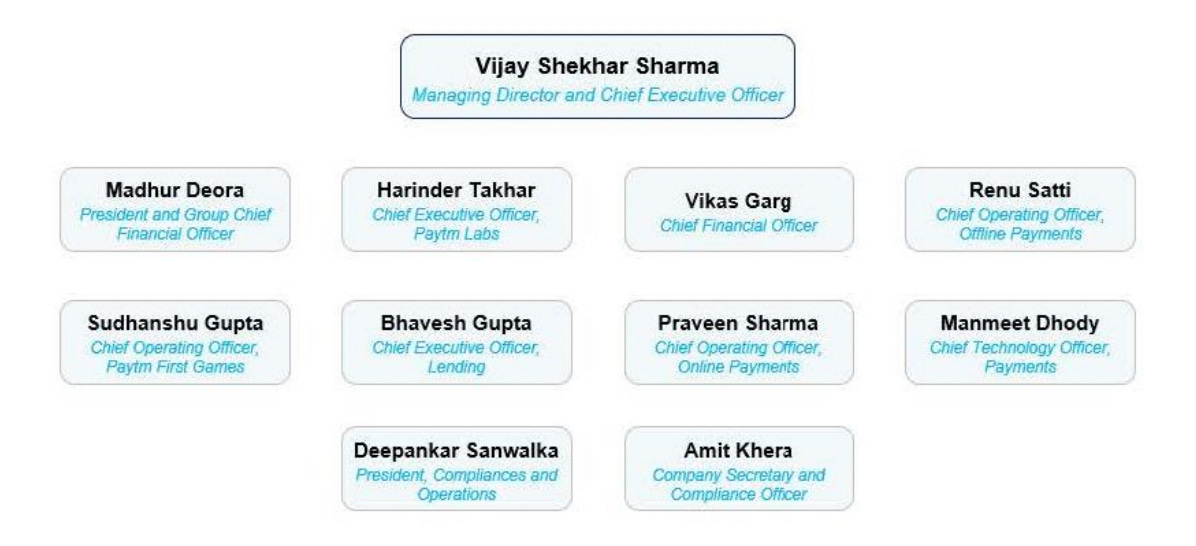

MANAGEMENT :

PAYTM GROUP COMPANIES :

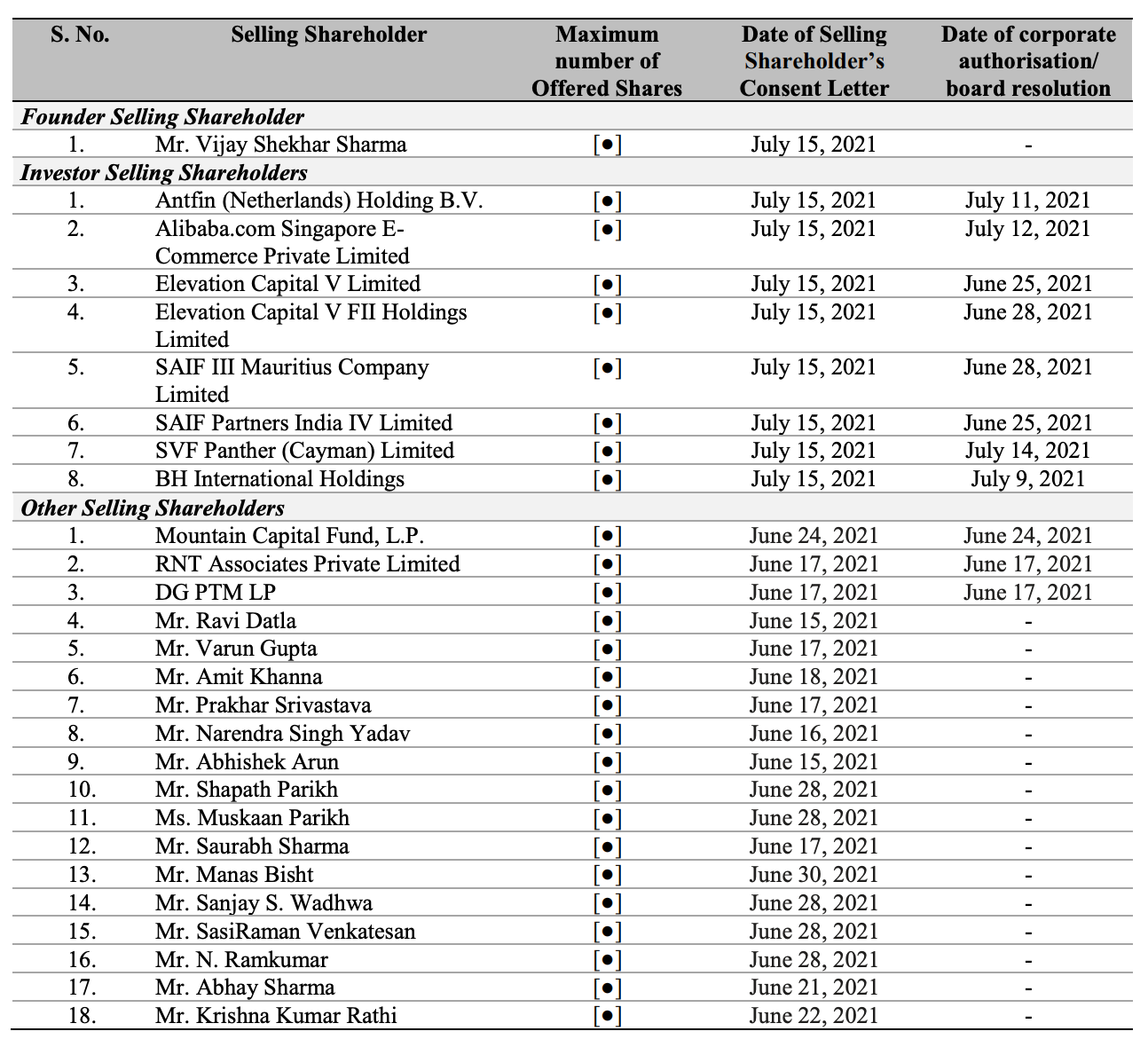

SELLING SHAREHOLDERS :

Let’s talk Financials :

PARAMETERS FY21 FY20 FY19 (in millions INR)

INCOME 31868 35407 35797

EXPENSE 47830 61382 77439

PROFIT/(LOSS) (15962). (25975). (41642)

PAYTM has Sanctioned DEBT of INR 15835 Million as of which the outstanding amount as of June 30, 2021, is INR 5432 Million.

GROSS MERCHANT VOLUME

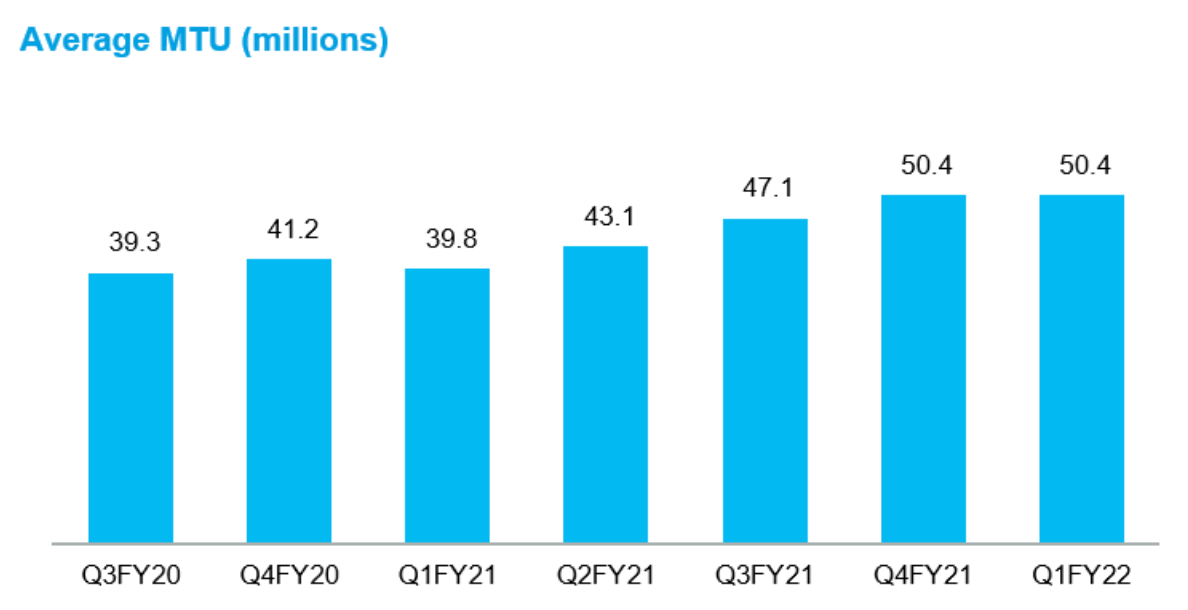

AVERAGE MONTHLY TRANSACTIONS

FINANCIAL SERVICES OFFERED –

COSTS :

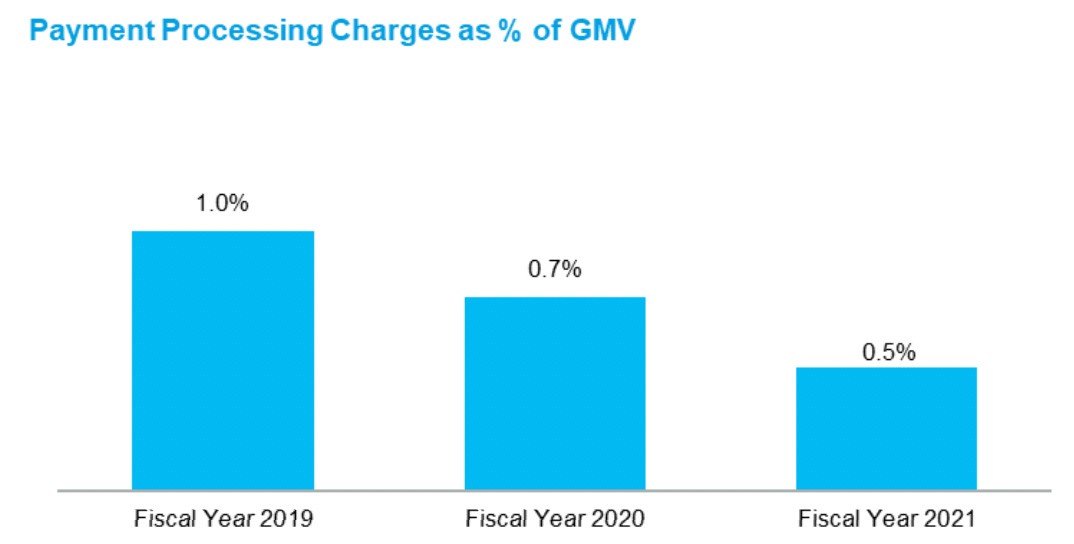

PAYMENT PROCESSING CHARGES :

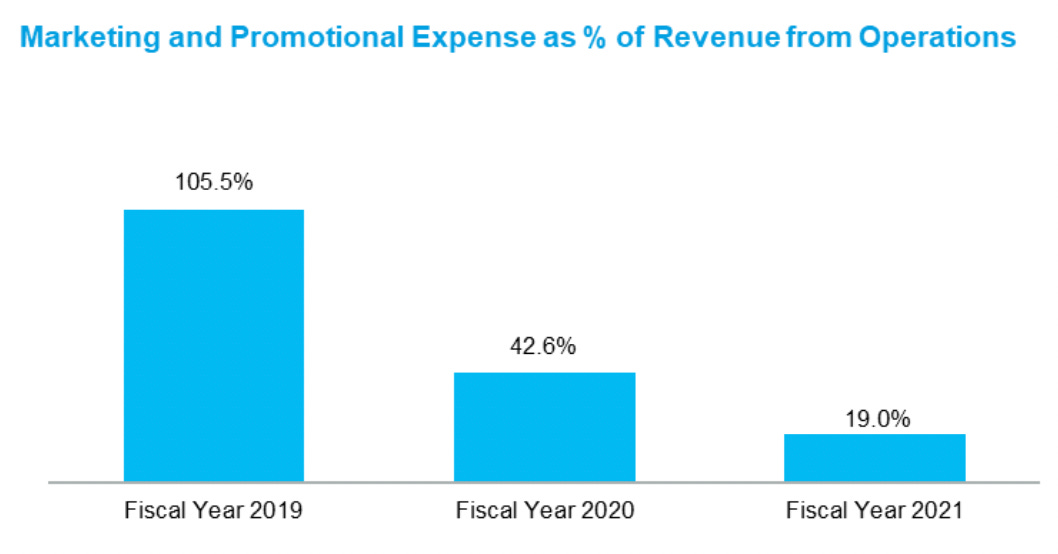

MARKETING & PROMOTIONAL EXPENSE :

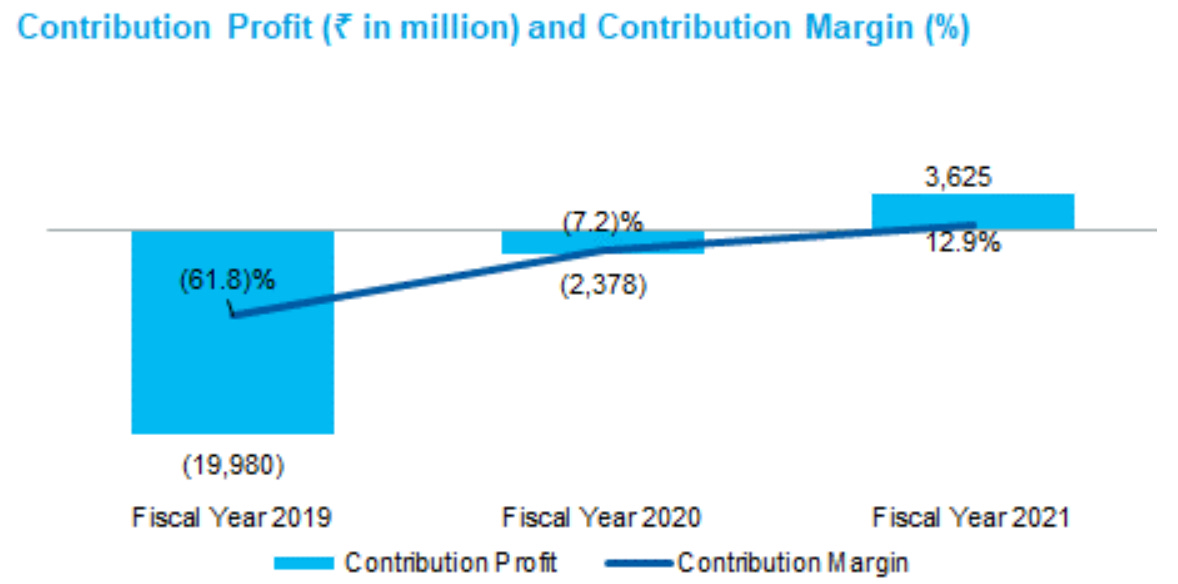

Improvement in Profit & Margins due to reducing cost :

So that’s how the PAYTM overall looks like.

My Remarks – Company has some solid plans for future growth. I am watching the company’s International Story as well as how they operate as a SMALL FINANCE BANK once they get approval. Also, most of the payments are done via PAYTM these days be it basic purchases or online shopping.

One key factor to look at here is how they become profitable from hereon. They are a still loss-making company and showing signs of lowering losses.

That’s it from my side guys.

See you in the next one.

Adios!